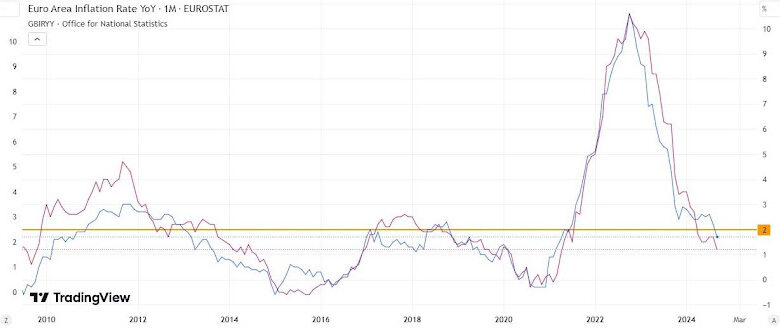

On Thursday, October 17th, the European Central Bank (ECB) cut interest rates by 25 basis points for the third consecutive time, as expected by most analysts. This move followed September data revealing inflation falling surprisingly below the official 2% target in both the Eurozone and the United Kingdom.

Signs of economic weakness continue in the Eurozone, with various economic indicators pointing towards a “stalling” economy, particularly in Germany. During the ECB board meeting in Ljubljana, Slovenia, President Christine Lagarde reiterated that a recession remains unlikely for now, although growth forecasts have been scaled back. She noted, “Lower confidence could prevent consumption and investment from recovering as fast as expected.”

There is a probability of another 25-basis-point rate cut in December, with expectations that rate cuts are likely to continue until late 2025. Despite positive inflation data bringing forward price target expectations, monetary easing is expected to persist, assuming the Middle East situation remains stable and oil prices do not surge.

Expectations for additional Fed rate cuts have eased across the Atlantic. With strong U.S. consumption and labor data, the dollar is anticipated to strengthen — a trend likely to persist as markets have already factored in the ECB’s recent rate cut. However, monitoring the economic calendar remains essential to stay informed about any events that might affect this outlook.

The market reaction was evident in the EUR/USD exchange rate, which dropped below its 200-period moving average on October 17th. The threat of trade tariffs promised by Donald Trump, the U.S. presidential candidate, could dampen global trade, forcing the ECB to extend its monetary easing policies to keep the euro competitive.

A strong dollar could jeopardize the stability of emerging markets and ripple through global trade. China’s central bank has promised economic support, but recent GDP data from China, showing slowing growth, have cast doubt. People’s Bank of China Governor Pan Gongsheng highlighted real estate and stock markets challenges as key factors requiring targeted policy support.

In this scenario, traders and investors have room to operate on both currencies, betting on a stronger dollar and a weaker euro, continuing a trend already underway — at least until parity is reached, which is currently seen as a long-term target.